Examining the Legal and Security Landscape Of Bearer Bonds

- 1 What Are Bearer Bonds?

- 1.1 Bearer bond benefits

- 1.1.1 Easily transferable

- 1.1.2 Anonymity

- 1.1.3 Fixed income

- 1.1.4 Lower capital loss risk

- 1.1.5 Anonymity

- 1.1.6 The risk of capital loss remains.

- 1.1.7 Potential theft/loss

- 1.2 The US Bearer Bond Policy

- 1.3 Face-value bearer bonds

- 2 Security for Bearer Bonds

- 2.1 Anonymity

- 2.2 Theft

- 2.3 Fraud

- 2.4 Record-Keeping

- 2.5 No Transparency

- 3 Most individuals encounter which bearer bonds?

- 3.1 Corporate Bearer Bonds

- 3.2 Municipal Bonds

- 3.3 Treasury Bearer Bonds

- 3.4 Bearer Savings Bonds

- 3.5 Bearer Bond Coupons

- 4 The Bottom Line

- 5 FAQs

In Short

- Bearer bonds are unusual financial instruments that need a bond certificate to redeem.

- Bearer bonds were previously common debt financing because they were easy to transfer and needed little administrative effort.

- Their usage has dropped considerably in recent decades because of the lack of registration, which encourages theft, money laundering, tax fraud, terrorist funding, and other crimes.

- They are practically gone in the U.S. and other advanced nations. Registered bonds, registered in a central database and transferred electronically, have replaced them.

Bearer bonds are financial instruments companies or governments issue to investors to finance various projects. The bond certificate and coupon bearer are not registered owners; they own the instrument and can claim its cash flows. Bearer bond coupons must be presented to the issuer or agent to receive interest payments. At maturity, you must provide the bond certificate to redeem it. This differs from registered bonds, which have electronically verified owners. Registered owners get a bond’s coupons and principal upon maturity. When a registered bond is sold in the secondary market, the stated owner is updated, and the new owner acquires cash flow rights. Bearer bonds can also be traded on the secondary market.

What Are Bearer Bonds?

Bearer Bonds operate similarly in that the bearer owns the bond. Whoever has the bond owns it. Whoever gives a bearer bond to the teller can cash it. Or compare it to dollars. A street-found Rs 2000 note belongs to the finder. The loser cannot recover it. Bearer bonds lack a stock exchange ownership record. Companies, municipalities, and other government entities can issue bearer bonds. Because bearer bonds have coupons, their interest is connected to the bond. The current bearer bond owner has to submit the coupon to the issuing corporation to get interest.

Bearer bond benefits

Easily transferable

People are used to rapid payments and remittances. Bank, trading, and demat accounts are opened in hours, and credit is available almost immediately. A bond that may be transferred instantly without paperwork or other transactions may be preferred by many investors.

Anonymity

Certain deals may be very confidential. Perhaps a person or organization does not want their employees to know about an external consultant engaged to assess their work. A government or police department may wish to engage someone to investigate corruption in their organization but does not want a paper record in case corrupt officials silence or intimidate them. Perhaps the bond seller/giver and bond receiver/buyer desire to keep confidentiality for other reasons, like Mrs. Kumar and her attendant Tina.

Fixed income

Bearer bonds pay monthly interest like other bonds. One of the bonds’ most popular features. The bond owner may earn a large recurring income from interest distributions, depending on the bond’s value and interest rate.

Lower capital loss risk

Many realize that bonds are safer than equities. A bond reflects a debt from the issuing corporation or government to the bondholder. The bondholder receives the value at maturity.

Anonymity

Anonymously paying auditors and investors or avoiding hungry heirs might help the unscrupulous launder money. Due to their popularity for money laundering, bearer bonds are outlawed in various nations.

The risk of capital loss remains.

The issuing corporation or government entity might choose not to pay the bondholder, especially if they lost money on the project or expansion they borrowed for. Government and muni bonds are less hazardous since investors don’t anticipate the government to steal their money.

Potential theft/loss

You couldn’t prove your bearer bonds were yours if someone broke into your home and took them, even if they were caught. If a fire, flood, or other calamity destroys the bearer bond, it’s lost.

The US Bearer Bond Policy

No legislation governs bearer bond issuance or transfer in the US. Instead, they tracked bearer bonds using the US Treasury Department, financial institutions, and law enforcement regulations. These guidelines simplify matters and reduce the chance of bearer bonds being used unlawfully. They instructed banking institutions to adopt stringent “know your customer” (KYC) and “anti-money laundering” (AML) processes while issuing and transferring bearer bonds to detect and prevent unlawful activity. The US Treasury Department has stopped issuing bearer bonds and mandated their conversion to registered bonds. Bearer bonds are less likely to be used illegally. Despite lacking a statute, US law enforcement extensively regulates and monitors bearer bond issues and transfers to avoid illegal usage.

Face-value bearer bonds

Bearer bonds have a face value, or par value, representing their maturity value. The bond issuer assures the bondholder the face value at maturity. The bondholder receives the face value, usually in dollars, if they retain it until maturity. Remember that bearer bond market value differs from face value. This relies on interest rates, issuer creditworthiness, and maturity time. Bond market values can rise or fall from their face values. Bearer bonds having a face value higher than their market value help issuers raise funds. It pays interest and returns the face value at maturity to bondholders.

Security for Bearer Bonds

Registered bonds offer higher security than bearer bonds; thus, they will ultimately replace them.

Important bearer bond security problems include:

-

Anonymity

Bearer bonds are actual certificates anybody may own. Without a registered owner or organization, finding them or halt fraud is hard.

-

Theft

Bearer bonds are tangible certificates that can be stolen and misplaced, making it impossible for the legitimate owner to recover their money.

-

Fraud

Anonymous bearer bonds make it easier for thieves to sell or transfer stolen bonds. Law enforcement has trouble finding and stopping such acts.

-

Record-Keeping

Bearer bonds must be maintained in one place, making it difficult for the issuer to track who is entitled to interest payments and principal at maturity. This raises default risk.

-

No Transparency

Bearer bonds have no central database. This hinders regulators and law enforcement from detecting and stopping money laundering and tax evasion. Bearer bonds are less popular due to security issues and will be replaced with registered bonds, which are registered in a central database and transferred electronically. It simplifies request tracking and prevents fraud and other crimes.

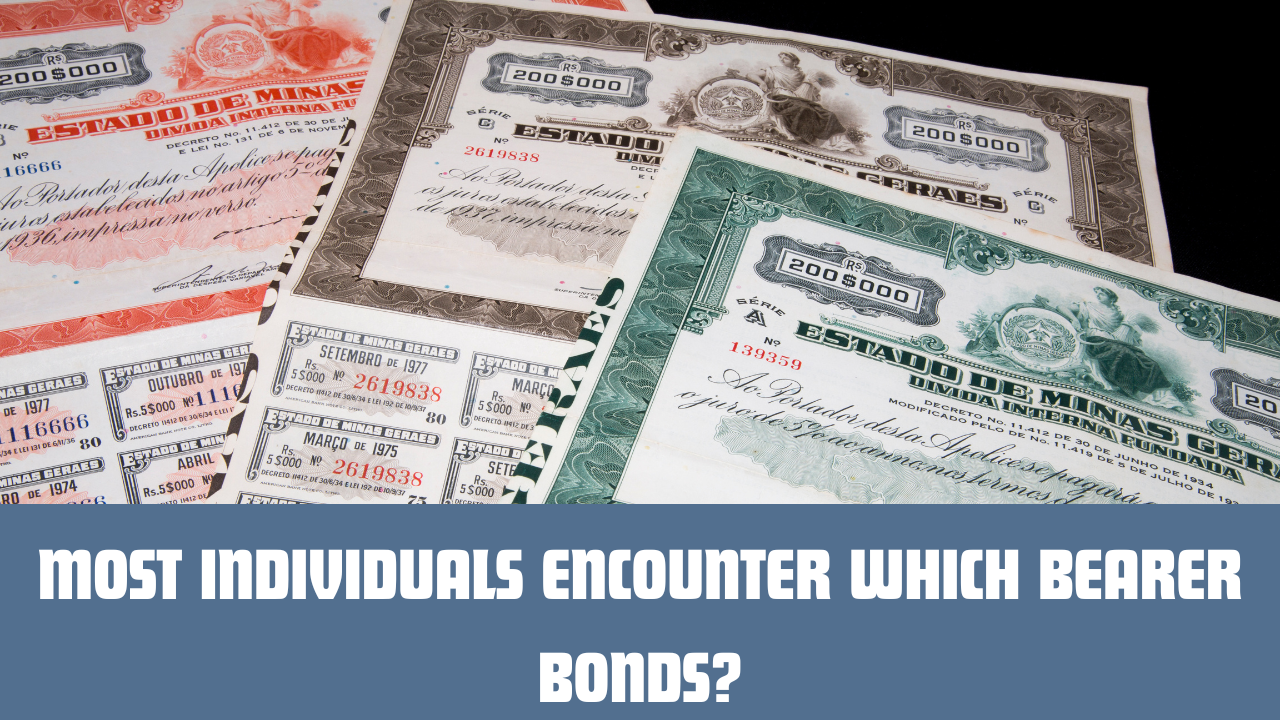

Most individuals encounter which bearer bonds?

Bearer bonds are unregistered debt securities. The holder of the bond certificate receives interest and principal payments as the owner. Most nations, including the US, no longer issue bearer bonds due to tax fraud, money laundering, and investor protection difficulties. Most people today seldom see bearer bonds. Historically, these bearer bonds were more common:

-

Corporate Bearer Bonds

These were issued by corporations to finance initiatives, growth, and acquisitions. Interest and principal payments were paid to the bondholder without registration.

-

Municipal Bonds

Municipalities issued these bonds to pay for road, school, and infrastructure improvements. Interest and principal were paid to the bondholder without registration, like corporate bearer bonds.

-

Treasury Bearer Bonds

The government issued these bonds to cover budget shortfalls or other public expenses. Since the government guaranteed them, they were low-risk investments.

-

Bearer Savings Bonds

These government-issued bonds for private investors have modest denominations and interest rates. Bearer savings bonds were used to save or donate money.

-

Bearer Bond Coupons

Bondholders clipped coupons from bearer bonds and presented them for interest payments until they were discontinued. Since they did not require registration and were payable to the person who submitted them, these coupons were bearer instruments.

Note: For the reasons noted above, most current bond offerings are registered, meaning ownership is recorded electronically or in other documents, and interest is paid directly to the registered owner.

The Bottom Line

Finally, a bearer bond demonstrates that the issuer owes the bondholder. Registered bonds are attached to a person or entity, unlike bearer bonds. Bearer bonds are tangible, unaffiliated certificates. They can be handed away by swapping the actual certificate. Recent security issues, including theft, fraud, and lack of transparency, have made bearer bonds less popular. They were replaced by registered bonds, owned in a central database, and transferred electronically. Some countries still trade and own bearer bonds. Law authorities strictly regulate and monitor their use to prevent money laundering and tax evasion. Bearer bond issuance and transfer are strictly regulated in the US. Financial institutions must follow stringent KYC and AML processes.

FAQs

What are Bearer Bonds?

Bearer bonds are unregistered financial instruments issued by enterprises or governments. The bond certificate holder owns and can claim cash flows.

How do Bearer Bonds Work?

Bearer bonds, like cash, belong to the owner. Present the actual certificate to redeem. Bearer bonds can be issued by enterprises and governments without stock exchange ownership records.

What Are Bearer Bond Benefits?

Bearer bonds are transferable, anonymous, pay interest, and have lower capital loss risk than shares.

What is Bearer Bond Capital Loss Risk?

If the financed project loses money, the issuing corporation may not pay the bondholder. Government and municipal bonds are safer.